Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

More Than a Yard: Finding the Right Home for Your Pooch

For many house hunters, a dream home isn’t complete without being a good fit for the family dog. Some might see the fenced in yard, and consider the box checked. However, if you are looking for your next home, you may want to look a little deeper to be sure the fit is right before signing on the dotted line.

It’s worth taking a little extra time to consider your pooch in a little more depth. Here is a quick checklist of considerations to be sure you find the right fit for your canine companion:

What’s in a Yard?

A fenced yard is, of course, ideal for many dog owners. It gives you the ability for off-leash play, a must for meeting the exercise needs of active breeds such as Border Collies or Labradors. But not all yards are the same. Here’s a quick checklist of what to look for:

- Check the fencing to be sure it is secure. Factor in any repair costs into the cost of the home since they will need to be addressed right away.

- Are there flower beds with potentially toxic plants that will need to be moved outside of the fenced area? Examples include many spring bulb favorites such as daffodils, tulips, and crocus, as well as some bushes such as azaleas.

- Is there a nice shady spot so your pooch can find shelter from the heat on a hot summer day?

- Is there access to water for an outdoor bath?

- Will delivery people be able to access your main entrance when the dog is outside without entering the fenced part of your yard? It is easy to overlook, but this can become a major annoyance if you do a lot of online shopping.

Indoor Space Considerations

It won’t always be a beautiful sunny day, even in your dream home. Make sure your new home will have enough space for a little indoor play on rainy days and during colder winter months. A long hallway can make a great runway for a game of fetch when getting outside just isn’t practical.

Likewise, consider the needs of aging or injured dogs. Does the layout of the home require going up and down stairs to get to the most used areas of the home? This can be a major problem for some special needs dogs, and a deal breaker for some pet owners.

Finally, most dog trainers recommend that every dog has a little space to call their own during times of stress. This may be as simple as a corner of the living room with a comfy dog bed or crate. If you have a puppy, however, a space that can be puppy-proofed and cordoned off (with appropriate flooring for potential accidents during potty training) is in order.

Go for a Walk

It may be impractical to include a dog walk for every home you look at while searching for your dream house. However, once you are down to a short list, it is time to actually take your dog on what is likely to be the daily walk route. Make sure this is a walk you would feel comfortable making every day, or even letting the kids take.

Be on the lookout for hazards: A dangerous intersection, a portion of the walk that requires walking in the road, or a neighbor who lets their dog run right up to the curb with invisible fencing (a recipe for territorial fights with leashed dogs passing by). A drive through is unlikely to reveal these walk spoiling annoyances. In addition, look for evidence of good lighting for evening or early morning walks.

Nearby Canine Amenities

If you are moving to a new part of town or relocating to a new state altogether, it is worth doing some research to find out where the pet services are located. Depending on the services you tend to use, it can make a big difference in your quality of life to be able to take advantage of nearby conveniences.

Think about what services you are likely to use most, and check on Google Maps to locate:

- Veterinarians

- Dog boutiques (particularly important if you buy specialty food)

- Grooming services

- Doggy daycare and boarding

- Pet sitting and dog walking services

- Dog-friendly restaurants (BringFido.comis a great research tool for this)

- Dog parks and dog-friendly paths for long walks

Flooring

Although luxurious hardwood flooring adds a great deal of ambiance to a home, it will have the opposite effect if it gets scratched up from the nails of a rambunctious canine. Large and even medium sized dogs can easily create unsightly scars in hardwood floors that can only be fixed by a professional who will need to sand away the wood then stain and refinish it. It’s a costly fix!

Modern carpets can generally hold up to doggy traffic. However, think about where you will be coming in and out of the house with your pooch to be sure you have a place to wipe muddy paws first on rainy days. A mudroom or garage entrance can easily stow a few extra towels for the job.

Tile and high-quality laminate flooring are the most durable as both will resist scratching and are easy to clean.

Consider Pet-Friendly Condos and Planned Communities

If you have a truly pampered pooch, one way to go the extra mile is to ask your realtor about dog-friendly communities in your area. Many condominium complexes, for example, have pet services right on site. Pet grooming, pet-sitting, dog walking services, and even a fenced in dog park and/or pool is available in some areas.

Work with a Knowledgeable Realtor

Make sure to let your agent know upfront that you have a canine member of your family to consider during the house hunt. If there are certain “musts” such as a fenced yard, or proximity to veterinary services, be sure to put that on the table upfront to help your realtor find a home that works for you and your furry friend.

Sharon is the lead author at wileypup.com. She received her M.S. in Science & Technology Studies from Virginia Tech and has worked as a professional dog trainer for over 10 years.

The Q4 2018 Western Washington Gardner Report

The following analysis of the Western Washington real estate market is provided by Windermere Real Estate Chief Economist Matthew Gardner. We hope that this information may assist you with making better-informed real estate decisions. For further information about the housing market in your area, please don’t hesitate to contact me.

ECONOMIC OVERVIEW

The Washington State economy continues to add jobs at an above-average rate, though the pace of growth is starting to slow as the business cycle matures. Over the past 12 months, the state added 96,600 new jobs, representing an annual growth rate of 2.9% — well above the national rate of 1.7%. Private sector employment gains continue to be quite strong, increasing at an annual rate of 3.6%. Public sector employment was down 0.3%. The strongest growth sectors were Real Estate Brokerage and Leasing (+11.4%), Employment Services (+10.3%), and Residential Construction (+10.2%). During fourth quarter, the state’s unemployment rate was 4.3%, down from 4.7% a year ago.

My latest economic forecast suggests that statewide job growth in 2019 will still be positive but is expected to slow. We should see an additional 83,480 new jobs, which would be a year-over-year increase of 2.4%.

HOME SALES ACTIVITY

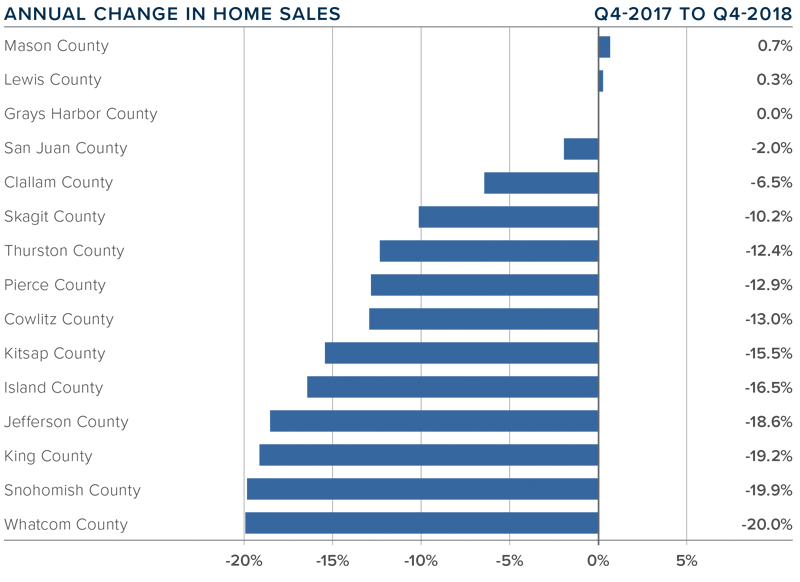

- There were 17,353 home sales during the fourth quarter of 2018. Year-over-year sales growth started to slow in the third quarter and this trend continued through the end of the year. Sales were down 16% compared to the fourth quarter of 2017.

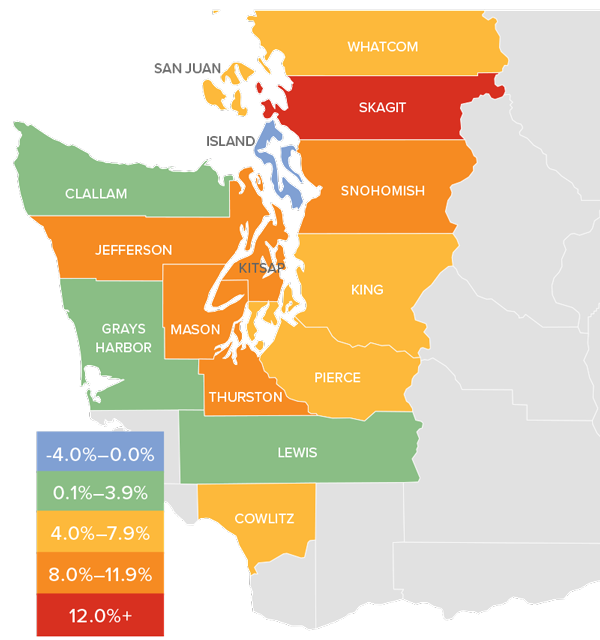

- The slowdown in home sales was mainly a function of increasing listing activity, which was up 38.8% compared to the fourth quarter of 2017 (continuing a trend that started earlier in the year). Almost all of the increases in listings were in King and Snohomish Counties. There were more modest increases in Pierce, Thurston, Kitsap, Skagit, and Island Counties. Listing activity was down across the balance of the region.

- Only two counties—Mason and Lewis—saw sales rise compared to the fourth quarter of 2017, with the balance of the region seeing lower levels of sales activity.

- We saw the traditional drop in listings in the fourth quarter compared to the third quarter, but I fully anticipate that we will see another jump in listings when the spring market hits. The big question will be to what degree listings will rise.

HOME PRICES

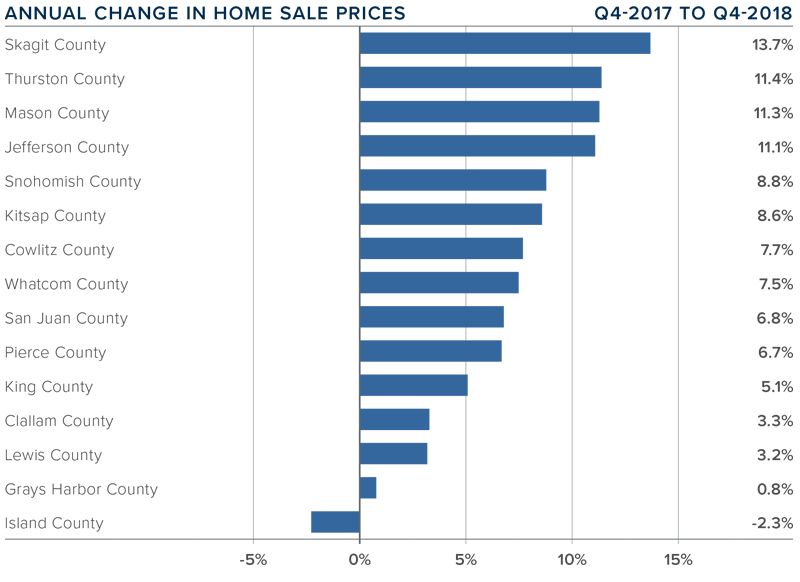

- With greater choice, home price growth in Western Washington continued to slow in fourth quarter, with a year-over-year increaseof 5% to $486,667. Notably, prices were down 3.3% compared to the thirdquarter of 2018.

- Home prices, although higher than a year ago, continue to slow. As mentioned earlier, we have seen significant increases in inventory and this will slow down price gains. I maintain my belief that this is a good thing, as the pace at which home prices were rising was unsustainable.

- When compared to the same period a year ago, price growth was strongest in Skagit County, where home prices were up 13.7%. Three other counties experienced double-digit price increases.

- Price growth has been moderating for the past two quarters and I believe that we have reached a price ceiling in many markets. I would not be surprised to see further drops in prices across the region in the first half of 2019, but they should start to resume their upward trend in the second half of the year.

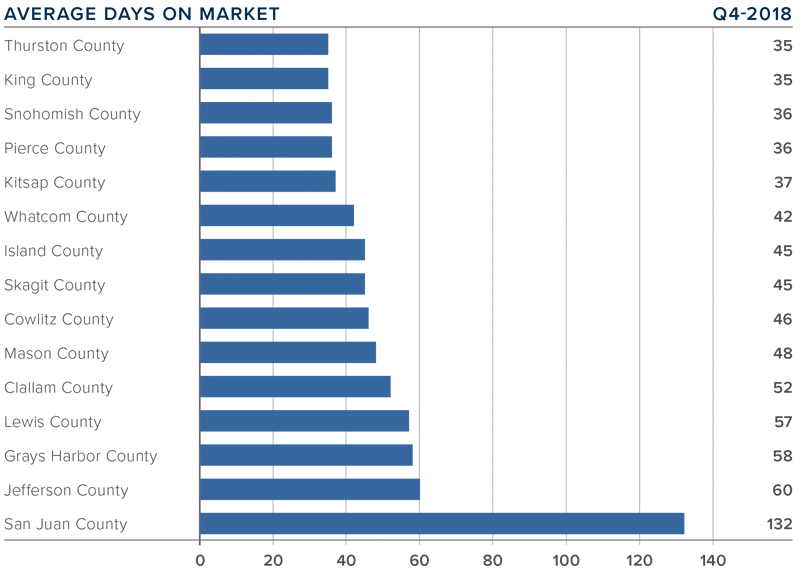

DAYS ON MARKET

- The average number of days it took to sell a home dropped three days compared to the same quarter of 2017.

- Thurston County joined King County as the tightest markets in Western Washington, with homes taking an average of 35 days to sell. There were eight counties that saw the length of time it took to sell a home drop compared to the same period a year ago. Market time rose in five counties and was unchanged in two.

- Across the entire region, it took an average of 51 days to sell a home in the fourth quarter of 2018. This is down from 54 days in the fourth quarter of 2017 but up by 12 days when compared to the third quarter of 2018.

- I suggested in the third quarter Gardner Report that we should be prepared for days on market to increase, and that has proven to be accurate. I expect this trend will continue, but this is typical of a regional market that is moving back to becoming balanced.

CONCLUSIONS

CONCLUSIONS

This speedometer reflects the state of the region’s real estate market using housing inventory, price gains, home sales, interest rates, and larger economic factors. I am continuing to move the needle toward buyers as price growth moderates and listing inventory continues to rise.

2019 will be the year that we get closer to having a more balanced housing market. Buyer and seller psychology will continue to be significant factors as home sellers remain optimistic about the value of their home, while buyers feel significantly less pressure to buy. Look for the first half of 2019 to be fairly slow as buyers sit on the sidelines waiting for price stability, but then I do expect to see a more buoyant second half of the year.

As Chief Economist for Windermere Real Estate, Matthew Gardner is responsible for analyzing and interpreting economic data and its impact on the real estate market on both a local and national level. Matthew has over 30 years of professional experience both in the U.S. and U.K.

As Chief Economist for Windermere Real Estate, Matthew Gardner is responsible for analyzing and interpreting economic data and its impact on the real estate market on both a local and national level. Matthew has over 30 years of professional experience both in the U.S. and U.K.

In addition to his day-to-day responsibilities, Matthew sits on the Washington State Governors Council of Economic Advisors; chairs the Board of Trustees at the Washington Center for Real Estate Research at the University of Washington; and is an Advisory Board Member at the Runstad Center for Real Estate Studies at the University of Washington where he also lectures in real estate economics.

2019 Economic and Housing Forecast

What a year it has been for both for the U.S. economy and the national housing market. After several years of above-average economic and home price growth, 2018 marked the start of a slowdown in the residential real estate market. As the year comes to a close, it’s time for me to dust off my crystal ball to see what we can expect in 2019.

The U.S. Economy

Despite the turbulence that the ongoing trade wars with China are causing, I still expect the U.S. economy to have one more year of relatively solid growth before we likely enter a recession in 2020. Yes, it’s the dreaded “R” word, but before you panic, there are some things to bear in mind.

Firstly, any cyclical downturn will not be driven by housing. Although it is almost impossible to predict exactly what will be the “straw that breaks the camel’s back”, I believe it will likely be caused by one of the following three things: an ongoing trade war, the Federal Reserve raising interest rates too quickly, or excessive corporate debt levels. That said, we still have another year of solid growth ahead of us, so I think it’s more important to focus on 2019 for now.

The U.S. Housing Market

Existing Home Sales

This paper is being written well before the year-end numbers come out, but I expect 2018 home sales will be about 3.5% lower than the prior year. Sales started to slow last spring as we breached affordability limits and more homes came on the market. In 2019, I anticipate that home sales will rebound modestly and rise by 1.9% to a little over 5.4 million units.

Existing Home Prices

We will likely end 2018 with a median home price of about $260,000 – up 5.4% from 2017. In 2019 I expect prices to continue rising, but at a slower rate as we move toward a more balanced housing market. I’m forecasting the median home price to increase by 4.4% as rising mortgage rates continue to act as a headwind to home price growth.

New Home Sales

In a somewhat similar manner to existing home sales, new home sales started to slow in the spring of 2018, but the overall trend has been positive since 2011. I expect that to continue in 2019 with sales increasing by 6.9% to 695,000 units – the highest level seen since 2007.

That being said, the level of new construction remains well below the long-term average. Builders continue to struggle with land, labor, and material costs, and this is an issue that is not likely to be solved in 2019. Furthermore, these constraints are forcing developers to primarily build higher-priced homes, which does little to meet the substantial demand by first-time buyers.

Mortgage Rates

In last year’s forecast I suggested that 5% interest rates would be a 2019 story, not a 2018 story. This prediction has proven accurate with the average 30-year conforming rates measured at 4.87% in November, and highly unlikely to breach the 5% barrier before the end of the year.

In 2019, I expect interest rates to continue trending higher, but we may see periods of modest contraction or levelling. We will likely end the year with the 30-year fixed rate at around 5.7%, which means that 6% interest rates are more apt to be a 2020 story.

I also believe that non-conforming (or jumbo) rates will remain remarkably competitive. Banks appear to be comfortable with the risk and ultimately, the return, that this product offers, so expect jumbo loan yields to track conforming loans quite closely.

Conclusions

There are still voices out there that seem to suggest the housing market is headed for calamity and that another housing bubble is forming, or in some cases, is already deflating. In all the data that I review, I just don’t see this happening. Credit quality for new mortgage holders remains very high and the median down payment (as a percentage of home price) is at its highest level since 2004.

That is not to say that there aren’t several markets around the country that are overpriced, but just because a market is overvalued, does not mean that a bubble is in place. It simply means that forward price growth in these markets will be lower to allow income levels to rise sufficiently.

Finally, if there is a big story for 2019, I believe it will be the ongoing resurgence of first-time buyers. While these buyers face challenges regarding student debt and the ability to save for a down payment, they are definitely on the comeback and likely to purchase more homes next year than any other buyer demographic.

Originally published on Inman News.

Mr. Gardner is the Chief Economist for Windermere Real Estate, specializing in residential market analysis, commercial/industrial market analysis, financial analysis, and land use and regional economics. He is the former Principal of Gardner Economics, and has more than 30 years of professional experience both in the U.S. and U.K.